The plays in the playbook: How advisers are structuring retirement approaches

By Mark Aldous | 14 May 2026 | 5 minute read

In our recent guide with Brooks Macdonald, ‘The CRP You Already Have’, we set out to help advice firms take a different look at how they approach consistency in retirement advice.

Rather than asking, ‘do you have a CRP?’, a question that can feel off-putting, we focus on something more practical. What does your retirement approach look like in practice and how consistent is it across your firm?

Most firms wouldn’t naturally describe this as a ‘playbook’, but when you step back from the day-to-day, patterns start to emerge. In how you evidence your clients’ understanding of risk in retirement, for example, or in how often and thoroughly drawdown clients should be reviewed. That’s the playbook.

The guide is structured around helping you strengthen the playbook. It will help you:

- Recognise the elements of a consistent retirement playbook that your firm already has in place.

- Identify the areas where firms most commonly have gaps.

- Work through the ten questions you need to answer before formalising your approach.

- Understand how the right approach varies by firm size and model.

This isn’t just about investment strategy. A strong retirement approach goes much wider, but in this blog I’m focusing specifically on how firms are structuring investment solutions within that broader picture.

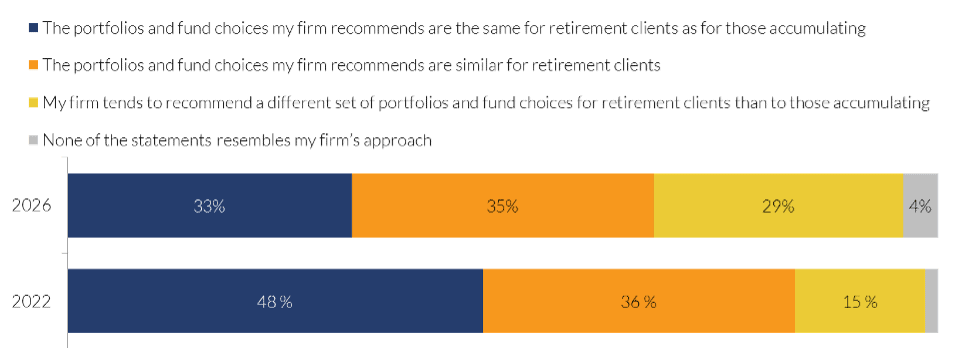

As part of the research we looked at how advisers are creating portfolios for their clients in retirement and the results point to a market in transition.

When we surveyed 223 financial advisers in early 2026, we found the profession divided almost evenly into three camps based on how advisers construct portfolios and funds for accumulation and retirement clients.

Figure 1 below shows the split between these approaches, with a large increase in the proportion of advisers recommending a different set of portfolios for retirement clients than accumulation clients. The proportion of advisers using entirely separate retirement portfolios has doubled since 2022, when it stood at just 15%. Advisers are shifting in how they are building retirement client investment portfolios, with fewer using the same portfolios and funds for retirement and accumulation clients.

Figure 1: Advice firm approaches to retirement client investment portfolios

Which one of the following statements, if any, resembles your firm’s approach to investment portfolios for retirement clients most closely? n=223

What really stands out is how strongly CRP adoption influences the approach to constructing retirement portfolios:

- Advisers working in firms with a formal CRP are more likely to use consistent, repeatable solutions: 42% use the same funds and portfolios across accumulation and decumulation, compared with 20% of advisers in firms without a CRP.

- Advisers in firms without a clearly defined CRP are more likely to use a mix of solutions, including smoothed funds, adviser-run portfolios, and multi-asset funds.

- Those working in firms with a CRP are more likely to use model portfolios and discretionary bespoke portfolios.

This research isn’t about one approach being right and another wrong. For advice firms still unsure about CRP adoption, the message from this research is a reassuring: you probably already have more of a consistent retirement playbook than you think. The more important question isn’t whether to build one. It is recognising what already exists, identifying the blind spots, and bringing the key elements together in a way that the whole firm understands.

Methodology:

These findings are based on research carried out by NextWealth including;

- Digital survey of 223 financial advisers offering retirement advice conducted during January and February 2026.

- Historic data from digital surveys of financial advisers in 2022, 2021 and 2020.

- Ten interviews with financial advisers and operations professionals representing a range of firm sizes and operating models, plus a compliance specialist and an outsourced paraplanning firm, conducted in January and February 2026.

Mark Aldous, Senior Quantitative Researcher at NextWealth

FAQS:

- What is a Centralised Retirement Proposition (CRP) and why does it matter for advice firms? A CRP is a consistent, firm-wide framework for how financial advisers approach retirement planning and investment for clients in drawdown. It matters because firms with a clearly defined CRP are more likely to use repeatable, consistent investment solutions — leading to better client outcomes and a more scalable advice process.

- How are financial advisers structuring retirement investment portfolios in 2026? Research from 223 financial advisers shows the profession is split almost evenly into three approaches: using the same portfolios for both accumulation and retirement clients, using entirely separate retirement portfolios, or using a mix of solutions. Notably, the proportion of advisers using separate retirement portfolios has doubled since 2022.

- Do advice firms need a formal CRP to deliver consistent retirement advice? Not necessarily. Many firms already have consistent patterns in how they approach retirement advice — from how they evidence client risk understanding to how frequently they review drawdown clients. The key is recognising what already exists, identifying the gaps, and bringing those elements together in a way the whole firm understands.

- What investment solutions are most commonly used for retirement clients? Advisers with a formal CRP tend to favour model portfolios and discretionary bespoke portfolios. Firms without a clearly defined CRP are more likely to use a broader mix, including smoothed funds, adviser-run portfolios, and multi-asset funds.

- How does CRP adoption influence retirement portfolio construction? Advisers in firms with a formal CRP are twice as likely to use consistent, repeatable investment solutions across accumulation and decumulation (42%) compared to those without one (20%). This points to a clear link between having a structured retirement proposition and greater consistency in how client portfolios are built and managed.