And behind door number four: the four PE exit routes for UK advice firms

By Alex Johnson | 14 May 2026 | 6 minute read

And behind door number four…

Shackleton’s agreement to acquire Hurst Point Group, parent of Argentis and Hawksmoor, is the largest UK advice-sector consolidation deal to date. Assuming the transaction completes, the combined business will hold approximately £17.5bn in assets under advice and management, serve more than 44,000 clients, and employ over 850 people including 233 FCA-authorised advisers and investment managers across 38 offices. NextWealth research shows it eclipses Titan Wealth’s January 2026 acquisition of Independent Wealth Planners (IWP), which added £6.9bn of client assets and took Titan to £44bn AUM.

The structure of the Shackleton–Hurst Point deal is also telling. Carlyle is not stepping away entirely: the firm plans to remain a minority investor in the combined Shackleton-Hurst Point Group alongside Lee Equity Partners. Hurst Point CEO Andrew Westenberger will join Shackleton’s executive committee on completion. That suggests Carlyle sees further value to be created in the combined group, rather than treating the transaction as a clean exit. It also points to a more flexible exit market, where PE investors may realise some value while staying exposed to the next stage of consolidation.

After a decade in which private equity poured capital into UK financial advice, a significant wave of investors is now looking for the door. The simple buy-and-build playbook of acquiring quickly, scaling EBITDA and selling on at a higher multiple is running out of easy road. Deals now need to be underpinned by strong governance and credible integration, with the FCA paying closer attention to how consolidation is delivered. Organic growth has also become a more important test of whether scale is creating real value.

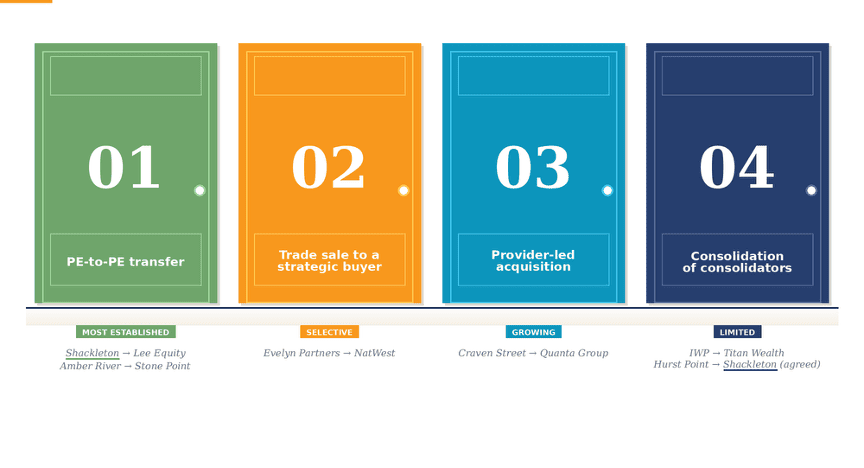

Our Consolidation of Advice Report 2026 identifies four main exit routes for private-equity-backed firms:

Figure 1: The four exit doors for PE-backed firms

What is behind each door

Door 1: PE-to-PE transfer

The most travelled path. Earlier or smaller PE owners sell to larger funds, often US-based, looking for scaled platforms in a maturing market. Sovereign’s exit of Shackleton to Lee Equity in 2025 fits the pattern. So does Penta’s part-exit of Amber River to Stone Point, although Penta remains invested.

Door 2: Trade sale to a strategic buyer

In the early 2020s trade sales were the default approach to acquisition. Aviva’s purchase of Succession, Schroders’ acquisition of Benchmark, and M&G’s acquisition of Sandringham and Continuum all sit here. Trade sales have become more selective. The agreed sale of Evelyn Partners to NatWest shows the route is not extinct, but still required effort as evidenced by Evelyn carving out professional services and direct-to-consumer brands first to make the wealth business cleaner to acquire.

Door 3: Provider-led acquisition

The route to watch. Quanta Group, which sits over Wealthtime, Copia Capital and Craven Street Wealth, is the clearest example of a platform-and-DFM owner buying its way into advice. Tatton’s backing of Absolute Financial sits in the same direction of travel. Also, while not explicitly a provider we hear that private banks are increasingly present in the bidding for advice firms.

“The two most interesting things are consolidators starting to consolidate each other, and banks re-entering the space. But stars need to align. You can’t force these things.”

– Private equity firm, NextWealth interview

Door 4: Consolidation of consolidators

This option has been widely discussed as the ‘end game’ option but it has thus far been limited largely because buyers risk inheriting unresolved integration, governance and funding problems. However, the Shackleton-Hurst Point deal demonstrates that it is viable option if the buyer believes the integration risk can be controlled.

What this means for the next 12 months

The pool of potential buyers is widening, not narrowing. Banks, DFMs, platforms, US private equity and established consolidators are all in the room. But the door is increasingly only open to firms that can evidence integration quality, clean data and organic growth, not just scale.

For PE-backed firms approaching the end of their hold period, the question is no longer whether there is a buyer. It is which of the four doors they qualify to walk through. Door number 4 is now open, but it is not wide. The firms most likely to pass through are those that can show they are already integrated, already governable and already capable of growing without another acquisition.

Get the full analysis

Consolidation of Advice Report 2026

The full report covers M&A activity in the UK financial advice market from Q1 2021 to Q1 2026, four distinct operating models acquirers are now building, how PE ownership is maturing, and detailed profiles of 30 leading acquirers. It is based on 22 in-depth interviews with acquiring firms, three interviews with PE investors, and NextWealth’s analysis of public transaction data.

The Consolidation of Advice Report is a paid research publication. Click here for more information.

Key takeaways

- Shackleton’s acquisition of Hurst Point Group creates a £17.5bn AUM advice business — the largest UK advice-sector consolidation deal to date.

- Carlyle is rolling over into a minority stake alongside Lee Equity rather than fully exiting — a hybrid PE structure becoming more common.

- NextWealth’s Consolidation of Advice Report 2026 identifies four main exit routes now available to PE-backed advice firms.

- Buyers are increasingly selective — integration quality, clean data and organic growth now define which exit doors stay open.

Alex Johnson, Head of data at NextWealth