The numbers that matter

By Julie Best | 26 March 2026 | 5 minute read

I try to work at my local gym once a week and do a training session at lunchtime. I’m good at ignoring Sky Sports, which plays silently on the screens.

Today, I was thinking about the numbers that matter to us.

Sahil Bloom describes five types of wealth: financial, time, mental, physical and financial wealth. Of these, financial wealth, by virtue of its number-based nature, is the most measurable, and therefore the one that gets the most focus. It’s not the only one that matters though, nor the only one that needs investment.

My eye is drawn to the tv and it’s because something is happening that I thought was abolished in the UK in 1834! People are being sold, one at a time, live, to the highest bidder in the room.

Those who follow cricket will of course recognise this spectacle as the inaugural Hundred Auction.

My first thought though: these are people! And they’re being very clinically reduced to a handful of numbers and bid upon.

I guess these are the right numbers if you’re assembling a winning cricket team: strike rate; matches played and so on.

What if you focused on the wrong ones?

The numbers we look at, and the ones we probably should.

When most people think about what a financial adviser does, they think: portfolios. Funds. Returns. Maybe charges.

This isn’t wrong, exactly. But it’s the equivalent of only looking at the batsman’s shoe size, or his number of Instagram followers.

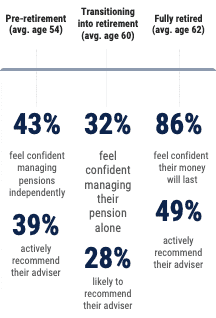

Our new retirement advice research, based on surveys of over 200 financial advisers, and 260 advised clients, reveals a different set of key numbers. And they tell a far more interesting story than just portfolio returns.

- Three quarters of advisers say their clients don’t accurately estimate what they’ll need in retirement

- Nearly half of clients underestimate what they’ll actually spend

- Only 28% of clients transitioning into retirement would recommend their adviser

- Yet once, they are fully retired, 86% of clients feel confident their money will last

At the very moment retirement becomes real, when the salary slows down or stops, big decisions need to be made and sense of self and identity shifts, client confidence in their adviser hits its lowest point. Once they’re through it, satisfaction strongly rebounds.

This is the confidence arc in retirement advice.

The work being done during the transition into retirement is hardest to assess at exactly the moment its potential value is greatest.

The normalising of huge uncertainty, stress-testing assumptions, reframing the, ‘what do I do with my pension’, question into a broader life question, is invisible to the client while they’re living through it.

“I had no idea this is what financial advisers do.”

A colleague recently showed a copy of our retirement advice report to a friend. The friend read it and said, genuinely surprised, “I had no idea this is what a financial adviser actually does. I thought it was just about choosing a portfolio.”

Our research shows exactly what advisers are doing. They’re helping a couple who are paralysed in planning their retirement by unspoken assumptions about what their adult children expect of them.

They’re convincing an elderly client that she can spend some of her wealth on double-glazing a draughty, old house. She can afford it. Her husband has Alzheimer’s and she doesn’t want to be forced to move him. Only for the adviser to be accused of being ‘a double-glazing salesman’ by a frustrated stepson who didn’t know the full story.

They’re sitting with someone who has £5 million after a divorce but feels destitute because other partners in his firm have twice that amount.

None of this shows up in the portfolio return and none of it is easy to measure.

The best retirement advice isn’t just about managing money; it’s managing the life the money is for.

(Finn Allen went for £160K, in case you’re wondering.)

Julie Best, Insight Director at NextWealth

FAQs

1. What are the “numbers that matter” in retirement planning?

The numbers that matter go beyond portfolio returns. They include how much you’ll spend in retirement, how long your money needs to last, and your confidence in financial decisions during the transition into retirement.

2. Why aren’t investment returns the most important measure of financial advice?

Investment returns are measurable, but they don’t capture the full value of advice. Financial advisers also help clients navigate uncertainty, make life decisions, and plan for spending—factors that aren’t reflected in performance figures.

3. What is the “confidence arc” in retirement?

The confidence arc describes how client confidence typically drops during the transition into retirement—when decisions are most complex—and then rises again once people are settled and reassured their finances will last.

4. Why do people miscalculate how much they need in retirement?

Many people underestimate both their future spending and the length of retirement. This is often due to uncertainty, lack of detailed planning, and difficulty visualising lifestyle changes.

5. What do financial advisers actually do beyond managing portfolios?

Advisers help clients make complex life decisions, manage emotional and family dynamics, plan spending, and build confidence about the future—not just select investments.