Should I stay or should I go? How do platforms and providers remain on panel?

By Alex Johnson | 16 July 2026 | 4 minute read

Platform and provider relationships with advice firms used to turn on price, functionality and service. Our latest research finds a fourth factor now decides who stays on a panel and who is asked to go: whether they can supply clean, consistent data. For consolidators in particular, data capability has become one of the clearest tests separating those that survive the cut from those that do not.

From nice-to-have to hard commercial requirement

Over the past two years we have heard from consolidators (in our Consolidation of Advice Report) that data access is a minimum requirement for an effective commercial relationship, not a differentiator. This year’s Data Openness research shows what that looks like in practice:

Firms are moving away from platforms and providers that cannot supply clear, timely and integrated data from panels and technology partnerships, regardless of price or relationship history.

“A key requirement of ours for any platform partnership is data access. If it’s not there, we don’t want to work with you.”

— Consolidator

Consolidators are leading the shift

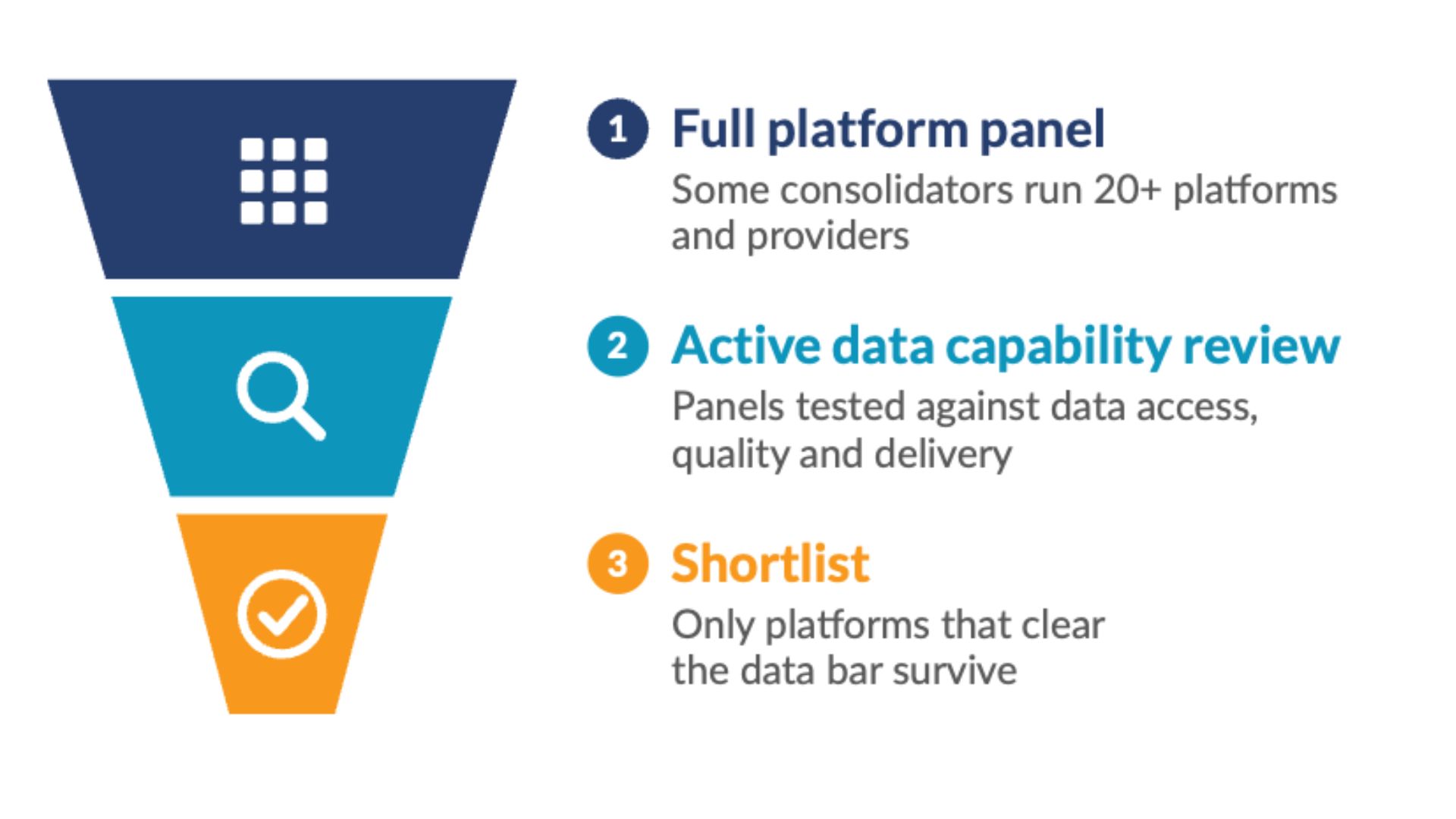

Consolidators are driving this change. Many are actively reducing the number of platforms they work with down to a shortlist panel. This is in part driven by a desire for better MI and private equity owners who want to better understand asset flows within the firm.

Planning-led firms are moving in the same direction, from an earlier starting point. Data is not yet triggering active switching for most of these firms, but it is becoming a stronger factor in where future business flows.

Data capability is reshaping platform panels

How consolidators are deciding which platforms and providers make the cut

“We’re on 20-something platforms. It’s crazy. We’ve got to get off them… We will consolidate on the ones that are the best at [data capability].”

— Consolidator

What this means for platforms and providers

The firms controlling the largest and fastest-growing pools of assets are making platform decisions based on data capability. That is not a future trend. This year’s interviews make clear it is happening now. Providers that want to be on the shortlist when consolidation decisions are made need to ask whether their current data offering is good enough to get them there.

Data capability sits alongside a wider set of gaps our research uncovered, including a universal problem with transaction data and a growing reliance on third-party aggregators to bridge what platforms and providers do not yet deliver. Our full report sets out where the largest commercial risks and opportunities lie.

Get the full analysis

The full report covers adviser satisfaction with platform and pension provider data across availability, quality, timeliness and delivery; the transaction data gap and why usability now matters more than availability; the data infrastructure reality across advice firms; the rise of the aggregation layer; and the commercial consequences for platforms and providers, including how consolidation is accelerating the shift. It draws on a survey of 201 advisers, nine in-depth interviews with technology and operations leaders at advice firms, and data requests from advice firms.

Click here for more information.

Alex Johnson, Head of Data

FAQs

Why has data capability become a consolidation issue?

Our Consolidation of Advice report 2026 found that data access is now a minimum requirement for an effective commercial relationship. Consolidators are removing platforms and providers that cannot supply clear, timely, integrated data from panels, regardless of price or relationship history.

How many platforms are consolidators trying to reduce to?

Some consolidators are actively reducing panels from 20 or more platforms and providers down to a shortlist. Data capability is a deciding factor in which platforms survive that process.

Are planning-led firms doing the same thing?

Planning-led firms are moving in the same direction from an earlier stage. Data is not yet triggering active switching for most, but it is becoming a stronger factor in where future business flows.

What should platforms and providers do about this?

Providers that want to be on the shortlist when consolidation decisions are made need to assess whether their current data offering, covering access, quality and delivery, is good enough to get them there.

What else does the Data Openness Report 2026 cover?

The report covers adviser satisfaction with platform and pension provider data, the transaction data gap, the reality of data infrastructure at advice firms, the rise of data aggregators, and the commercial consequences of data for platforms and providers.